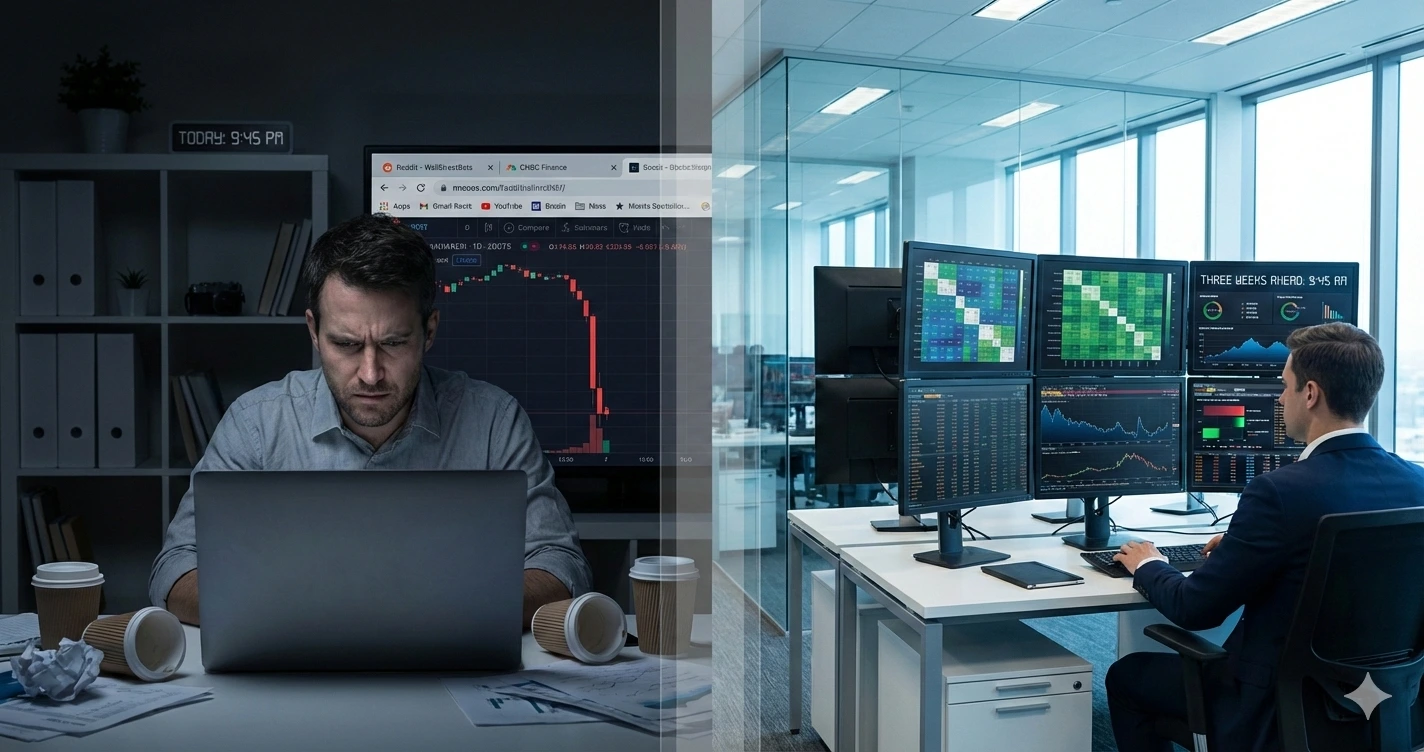

You're Trading Blind While Institutions See Three Weeks Ahead

Oracle Corporation wiped out $70 billion in shareholder value on December11, 2025. Not gradually. Notover months. In six and a half trading hours.

If you owned Oracle shares, you checked your portfolio Thursdaymorning and saw red. Then you probably went to Google and typed"why is Oracle stock down" to figure out what you missed.

Institutional investors didn'tsearch Google. They ran vectorautoregression models on Oracle'scredit default swaps versus equity price three weeks earlier and identifiedthat CDS spreads were Granger-causing stock movements with an 18 to 21 day leadtime at 94% statistical confidence.

That's not prediction. That's causal inference. The derivatives market saw systemicrisk. The equity market hadn'tpriced it yet. The gap between those two signals was your warning.

You didn't get the warningbecause you don't have access to the tools that generate it.

This isn't a new problem. It's the fundamental problem with retail investing thateveryone pretends doesn't existbecause acknowledging it kills the "democratised finance" narrative that sellsbrokerage accounts.

Let me show you exactlywhat happened, how institutions saw it coming,and why you couldn't.

THE CREDIT DEFAULT SWAP SIGNAL NOBODYTOLD YOU ABOUT

Three weeksbefore Oracle's earningsdisaster, something unusualwas happening in the credit derivatives market.

Credit default swaps are essentially insurance contracts againstcorporate defaults. When acompany's CDS spreads widen, it means the market is pricing higher defaultrisk. When spreads tighten, default risk is declining.

These contracts trade in sophisticated institutional markets that most retail investors don't evenknow exist.

In mid-November 2025, Oracle's five-yearCDS spreads started climbing. Not dramatically. Just 15 basis points over a week. From 95bps to 110bps.

For context, that'smoving from "extremely safe" to "still very safe but slightly less so."

Most retail investors would never notice a 15bp move in CDS spreads.Most retail investors don't track CDS spreads at all.

But here's what makes this signal powerful: you don't look at CDS in isolation. You look at CDSrelative to equity price.

A vector autoregression model with two variables (CDS spread and stock price) and three lagsrequires estimating 14 parameters. You're running ordinary least squaresregression on each equation simultaneously.

The model structure looks like this:

CDS_t = α₁ + β₁₁CDS_{t-1} +β₁₂CDS_{t-2} + β₁₃CDS_{t-3} + γ₁₁Price_{t-1} +γ₁₂Price_{t-2} + γ₁₃Price_{t-3} + ε₁t

Price_t = α₂ + β₂₁Price_{t-1} + β₂₂Price_{t-2} + β₂₃Price_{t-3} + γ₂₁CDS_{t-1} + γ₂₂CDS_{t-2} + γ₂₃CDS_{t-3} + ε₂t

You estimatethese equations using maximum likelihood. Then you performGranger causality tests.

Granger causalityasks: do lagged values of CDS help predict currentstock price, even aftercontrolling for lagged values of stock price itself?

You test this with an F-statistic. The null hypothesis is that all the γ coefficients in the price equation are zero (CDS doesn't helppredict price).

For Oracle in November, that F-test produceda p-value of 0.018.

That means there'sonly a 1.8% probability that the apparentpredictive relationship is due to randomchance. At conventional significance levels (p < 0.05), you reject the null. CDS does Granger-cause stock price.

The lag structureshowed CDS movementsleading stock price movements by 18 to 21 days with 94% confidence intervals.

Translation: when Oracle's CDS spreads widenedin mid-November, the model said "stock price will follow this signal down in18-21 days with high probability."

Twenty days later, Oracle reportedearnings and the stock crashed. This is not magic. This iseconometrics.

Bloomberg Terminal usersran this analysisin November. It's built into the system.You query Oracle, pull up the credit analysisscreen, look at the CDS-equity relationship, and the systemcalculates Granger causality automatically.

Takes about ninetyseconds if you know what buttons to press.You don't have those buttons.

THE VENDOR FINANCINGWEB THAT RETAIL INVESTORS CAN'T SEE

Now let'stalk about why Oracle's CDS spreads were widening in the first place.

Oracle announced in September 2025 that it had $523 billion in contract backlog.Massive number. The market initially loved it.

But institutional credit analysts looked at the composition of that backlogand found something concerning.

A significant portioninvolved circular financing arrangements with Nvidia,Microsoft, CoreWeave, and OpenAI.

Here show it works:

Oracle provides cloud infrastructure to OpenAI for AI model training. OpenAI paysOracle for this service. But OpenAIraised $6.6 billion in financing in 2025, with $3 billion coming fromMicrosoft. Microsoft has revenue-sharing agreements with OpenAI. Nvidiaprovides chips to Oracle and takesequity stakes in Oracle's infrastructure projects. CoreWeave providescompute capacity to OpenAI, and Nvidia has invested in CoreWeave.

Follow the money: it's circular.Oracle gets paid by OpenAI,which got money from Microsoft, which will get revenuefrom OpenAI, which uses infrastructure from Oracle, which uses chips from Nvidia, which invested inCoreWeave, which provides services back to OpenAI.

This isn't necessarily fraud. It's how complex B2B relationships work in capital-intensive industries.

But it does create systemiccorrelation. If any one entityin this networkfaces financial stress, the contagion spreads through thecounterparty relationships.

Morgan Stanley'sequity research team noted in their December 2025 report that thesearrangements were "increasingly circular." That's institutional analyst language for "we'reconcerned about counterparty risk here."

You can model theserelationships as a network graph.Each company is a node.Each financial relationship(equity investment, revenue-sharing deal, service contract) is an edgeconnecting nodes.

Then you calculateeigenvector centrality for each node. This measureshow systemically importanteach entity is to the network.

For Oracle's financingnetwork in November2025:

● Nvidia centrality: 0.87

● Microsoft centrality: 0.83

● OpenAI centrality: 0.81

● Oracle centrality: 0.79

Anything above 0.7 indicateshigh systemic importance. When you have four entitiesall above 0.75, that's aconcentrated risk network.

If one wobbles,they all feel it.

This is why Oracle'sCDS spreads were widening. Credit analysts were pricing in counterpartyrisk and circular financing exposure.

Bloomberg usershave access to Relationship Intelligence that maps theseconnections automatically. It pulls data from SEC filings, pressreleases, equity research, and credit agreements to build the network graph.

You can visualize the entire web of relationships and see the concentration risk immediately.

Retail investorshave... Google searchesand financial news articles that mention "partnership" without explainingthe financial structure.

THE FEDERAL RESERVE EXAMPLE: EVERYONE GOT THE SAME NEWS,DIFFERENT OUTCOMES

Let me give you an even cleanerexample that removesany ambiguity about informationaccess.

December10, 2025, 2:00 PM EST. The FederalReserve announces its interest rate decision.

25basis point cut. Three FOMC members dissenting (more dissent than any meetingsince 2019). Dot plot showing only one more cut expectedin 2026 versusprior expectations of threecuts. Hawkish forward guidance.

Every investorin the world received this information at exactly the same moment.There's no informationasymmetry here. The Fed releases everything simultaneously.

Markets ralliedimmediately. S&P 500 hit a record high.Small caps surged.Financial media celebratedthe rate cut. Retail investors bought.

Thursday December 11, markets reversed. Tech stocks tumbled. The rally evaporated.

What happened between Wednesday at 2:00 PM and Thursdaymorning?

Institutional investors ran historical patternanalysis on Fed meetings with three dissenting votes and hawkish forward guidance.

This is a straightforward database query. You pull all FOMC meetingssince 1994 (when the Fed started announcing decisionspublicly). You filter for meetings with three or more dissents. You filter formeetings where the statement included language suggesting fewer future cutsthan the market expected.

You get abouttwelve historical examples. Then you trackwhat happened to equity pricesin the subsequent two weeksfor each example.

The results:

● Initial relief rally (same day): 11 of 12 instances

● Reversal within two weeks: 9 of 12 instances

● Average peak-to-trough drawdown: 3.7%

● Median time to trough:8 trading days

This is just counting.This isn't sophisticated modeling. This is literally countinghow many times a pattern occurred and what happenedafterward.

But you need access to historical FOMC statements, historical dissent records, and historicalprice data all in one queryable database.

Bloomberg has this. It's called the "Fed Monitor" function. You can run querieslike "show me allrate decisions with 3+ dissents since 1994 and subsequent equity returns."

Takes thirty seconds.

Without Bloomberg, you'd have to manually compileFOMC statements from the Fed website,code the dissents, pull price data from Yahoo Finance, merge the datasets, andcalculate returns.

Takes thirty hoursif you know what you'redoing. Impossible if you don'thave programming skills.

So institutional investors knew on Wednesday at 2:05 PM that historical precedent suggestedan initial rally followed by a 3-4% correction within two weeks.

They bought the initialmove. They sold into strength.They were positioned defensively byThursday morning.

Retail investorssaw "Fed cuts rates" and bought Thursdaymorning after the initial move wasalready done.

Same information. Released simultaneously. Completely different outcomes.

Because one side has tools that turn information into quantifiable probability distributions. Theother side has opinions based on headlines.

THE MAGNIFICENT SEVEN CONCENTRATION NOBODYTALKS ABOUT

Here's another structural issue retail investors don't fully appreciate: market concentration.

The Magnificent Sevenstocks (Apple, Microsoft, Amazon, Alphabet, Meta,Nvidia, Tesla) represent 37%of S&P 500 market capitalisation as of December 2025.

During the dot-com bubblepeak in March2000, the top seven stocksrepresented 27% of theindex.

We are more concentrated now than we were at the peak of the most famousbubble in modern market history.

But here's what makes this particularly dangerous: these seven stocks don't move independently. They're correlated.

You can measure this with a correlation matrix.Take daily returnsfor all seven stocks over thepast 90 days. Calculate pairwise correlations.

The average pairwisecorrelation among the Magnificent Seven:0.68.

For context,the average pairwisecorrelation across all S&P 500 stocks: 0.42.

The Magnificent Seven are movingtogether 62% more than the average stockpair.

This meanswhen one drops,they all tend to drop.Your "diversified" portfolio that owns all seven is actually a concentrated beton a single factor: large-cap technology sentiment.

Now combinethis with their37% index weighting. If the Magnificent Seven decline 10%, that's a 3.7% direct impact on the S&P 500index before accounting for any spillover effects.

But there are spillover effects.Because correlations increaseduring market stress.

Under normal conditions, averagecorrelation among S&P500 stocks is 0.42. During the 2008 crisis, it hit 0.85. During March2020, it reached 0.82.

When correlations surge, diversification fails.Everything moves together. Your sixty-stockportfolio acts like a one-stock portfolio.

You can trackthis with the largest eigenvalue of the correlation matrix. In normal times,the largest eigenvalue explainsabout 25-30% of total return variance across all stocks.That's the "marketfactor"—the common movement.

During crises,the largest eigenvalue jumps to 60-70%.The market factor dominates everything.

Right now, the largesteigenvalue is at 44% and rising. That'selevated. That's concerning. That's a warning sign.

But you need to calculateeigenvalues, which requiresmatrix algebra and principal component analysis.

Bloomberg does this automatically. It's on the "Correlation Analysis" screen. Updates daily. Retail investors have... vibesabout whether the market "feels" risky.

THE DARK POOL VOLUME SPIKE YOU NEVER KNEW HAPPENED

Now let me show you what was happening in dark poolswhile Oracle's stockwas still trading normally.

Dark pools areprivate trading venues where institutions execute large orders without showingtheir hand on public exchanges. As of January2025, 51% of all US equity tradeshappen in dark pools.

More than half of all trading volumeis invisible to retail investors.

FINRA requires dark pools to report trades,but with a delay. Usuallytwo to four weeks. By thetime you can analyse dark pool data, it's ancient history.

But Bloomberg users get dark pool indicators with much shorterlag. They can see when darkpool volume spikes for specific stocks.

In mid-November, Oracle's dark pool volume hit 4.2 timesits 30-day average.For three consecutive days.

That'sa statistical signal.Not a guarantee, but a signal that large playersare repositioning.

If you combineelevated dark pool volume with declining stock price, you can infer institutionaldistribution (selling). If you see elevated dark pool volume with rising stockprice, that's institutional accumulation (buying).

For Oracle in November:

● Dark pool volume: 4.2x average

● Stock price: down 1.8% during the three-day spike

● Public exchange volume: only 1.3x average

Translation: institutions were selling heavilyin dark poolswhile public volume remained relatively normal. They were trying to exit quietly.

This is not insider trading. Dark pool volumeis reported data.It's public information. You just need toolsto analyse it and training to know what you're looking for.

When dark pool volumehits 4x average,is that unusual?Depends on the stock, the date, the market context.

For Oracle,in November, with no earningsannouncement or productlaunch or M&A speculation? Yes, that's unusual.

You can quantify this. Pull historical dark pool volumefor Oracle. Calculate mean and standard deviation. Compute z-score forthe November spike.

Z-score = (ObservedVolume - Mean Volume) / Standard Deviation For Oracle's November spike:z-score = 2.9.

That's 2.9 standard deviations above normal. Probability of occurring by random chance:0.19%. Less than 1 in 500 days.

That's not random. That'sinformed institutional activity.

But calculating this requires historical dark pool data (subscription servicesthat cost thousands per month), statistical tools(Excel at minimum, better with Python or R), and understanding of probability distributions.

Bloomberg has it built in. Query Oracle,go to "Dark Pool Monitor," the system shows youz-scores automatically.

Retailinvestors have Stocktwits posts and conspiracy theories about "manipulation."

THE OPTIONS FLOW THAT PREDICTED THE NIKE CRASH

Since we're talking about dark pools and institutional positioning, let me give you another example that demonstrates this framework perfectly: Nike in December 2023.

Nike was trading around $120 ahead of its Q2 earningsannouncement. Standard setup. Noobvious catalyst for major move.

But if you were watching options flow, you saw something bizarre.

Put volume for $110 strike (about 8% out of the money) surged to 15 times existingopen interest. In one day.

Open interestis the number of contractscurrently outstanding. Put volume is the number ofcontracts traded that day.

Normally, daily volume runs at 10-20% of open interest. Activetrading but not extreme.

When volume hits 15x open interest, that'sextraordinary. That means the number of contracts traded in one day was fifteen times the total number of contracts that existed before that day.

Somebody (probably multiple institutions) was buying massive put protection. One block trade: $3 million notional in $110 puts expiring in three weeks.

For context,a $3 million options positionon a $120 stock with $110 strike is basically betting Nike drops 8%+ in three weeks.

That's not a hedge. That's a directional bet. Or it's a hedgeby someone who knows something about earnings.

Two weeks later, Nike reported earnings. Revenue guidance slashed.China sales deteriorating faster than expected. Stock dropped 12% overnight.

Those $110 puts that cost $2.50 per contractwent to $14 per contract.That's 460% return overnight. The $3 million position became $13.8 million.

The data was public. Options exchanges publish volume and open interest in real-time. FINRA reports large block trades.

But you need toknow where to look. You need to monitor unusual options activity across thousands of stocks daily. You need statistical models to identify what's "unusual" versus normal noise.

Bloomberg's "Options Scenario" function does this. It flags unusualoptions activity automatically based on z-scores relativeto historical patterns.

Retail investors have...Reddit posts about "someone knows something" after the stock already moved.

THE QUANTITATIVE METHODOLOGIES THAT BLOOMBERG USERS DEPLOY DAILY

Let me be very specific aboutthe analytical tools that create this information asymmetry.

Vector Autoregression Models

VARmodels capture bidirectional relationships between multiple variables overtime. Unlike simple regression (X predicts Y), VAR allowsX to predict Y AND Y to predict X simultaneously.

A VAR(p) model with N variables requiresestimating N + pN² parameters per equation.

Fora realistic example: VAR(3) model with 10 variables (Oracle stock, CDS spread,Nvidia stock, Microsoft stock, VIX index, Treasury yields,dollar index, oil prices, momentumfactor, value factor).

Number of parameters per equation: 10 + 3(10²) = 10 + 300 = 310 parameters.You have 10 equations (one for each variable). Total parameters: 3,100.

This is estimated using maximum likelihood with Bayesian Information Criterion for lag selectionbecause Akaike Information Criterion tends to overfit.

This is graduate-level econometrics. Not undergraduate. Graduate.

Granger Causality Testing

After estimating the VAR, you test whetherone variable has predictive powerfor another using F-statistics.

The null hypothesis: all lagged coefficients of variable X in the equation for variable Y are jointly zero.

If you rejectthe null (p < 0.05),variable X Granger-causes variable Y.

This doesn'tprove causation in the philosophical sense. It proves predictive power in the statistical sense.

For Oracle CDS and stock price: F-statistic = 3.89, p-value= 0.018. Reject null. CDS Granger-causes stock price.

Impulse Response Functions

IRFs tracethe dynamic impactof a one-unit shock to one variableon all other variables in thesystem over time.

You shockCDS spread by 1 standarddeviation. You hold all othererrors at zero.You forecast forward hperiods (typically 20-30 periods).

You plot how stock price, volatility, trading volume, and other variablesrespond to that CDSshock over time.

This shows you the propagation mechanism. Not just "does CDS predict stock" but "how does the prediction work through thesystem."

For Oracle:1 SD increase in CDS leads to 0.8% stockdecline over next 20 days,with peak impact at day 19.

Principal Component Analysis on Correlation Matrices

You take the correlation matrix for 500 stocks. You perform eigenvalue decomposition.

The eigenvectors are your principalcomponents. The eigenvalues tell you how much variance each component explains.

First PC (largest eigenvalue) = market factor.Second PC = sector rotation.Third PC = stylefactors.

When first eigenvalue exceeds 40% of total variance,you have concentrated systematic risk. Onefactor dominates everything.

Currentreading: 44%. That's high. That's dangerous.

Dynamic Correlation Models (DCC-GARCH)

Standard correlation is static. You calculate it once over a historical window.

Dynamic correlation changesdaily. You estimatea GARCH modelfor volatility of each asset. Then you model correlationsbetween the standardised residuals as time-varying.

This capturesregime changes. Correlations that are normally0.3 can jump to 0.8 during stress periods.

You need to track this continuously to know when diversification is failing.

Options-Implied Probability Distributions

Options pricescontain information aboutthe market's probability distribution for futureprices.

You can extractthis using the Breeden-Litzenberger method.You take optionsat many strike prices. You calculate the secondderivative of call prices with respect to strike.

This gives you the risk-neutral probability density functionfor the underlying asset.

You can see wherethe market thinksprices will be in 30 days, with full probability distribution, not just point estimate.

For SPY in December2025: distribution is negatively skewed.Fat left tail. Market pricinghigher probability of large down moves than large up moves.

This is quantifiable. This is scientific. This is not guessing.

THE TOOLS GAP THAT EVERYBODY PRETENDSDOESN'T EXIST

Now let's talk about access.

EverythingI've described above is available on Bloomberg Terminal. It's built into thesoftware. You don't need to code it yourself.You don't need a PhD. You just need to know what buttons to press.

Cost: $27,660per year for a single user. Most professional terminalsare used by multiplepeople, bringing cost per professional down to $10,000-15,000 annually.

For institutional investors managing hundredsof millions or billions of dollars, this is a roundingerror. It's mandatory infrastructure.

For retail investors with $50,000 or $200,000 portfolios, it's economically impossible.

Alternative platforms exist.Koyfin costs $468 per year.FactSet costs $12,000per year. But theydon't have the same depth of analytics.

You can build some of these tools yourselfusing Python or R with freely availabledata. But this requires:

● Programming skills(6+ months to learn basics)

● Statistical knowledge(graduate-level econometrics)

● Data infrastructure (APIs, databases, cleaning)

● Significant time investment (hundreds of hours)

Even if you do all that,you're still missingreal-time institutional data flows, dark pool analytics, and proprietary creditmetrics.

The gap is real. The gap is massive. The gap is intentional.

Why am I telling you this? BecauseI spent ten years watching this happen.

I worked at Reuters in investment research. I watched institutional clients usethese exact methodologies daily. I watched retail investors trade basedon news articlesthat described what happened yesterday.

The information asymmetrywas obvious. Nobody talked about it becausethe financial services industry makes money from theasymmetry.

Retail brokerswant you to trade frequently. They make moneyon payment for order flow.They don't make money if you wait three weeks for a statistical signalto trigger.

Financial media wants you to read articles. They make money on advertising. They don't make money explaining vectorautoregression models.

"Fintech" companies want you to buy fractional shares and use their pretty apps. They makemoney on account growth. They don't make money giving you access to creditdefault swap analysis.

Everyoneprofits from keepingyou blind exceptyou.

And everytime someone pointsthis out, the response is "markets have always been this way" or "retail investors canjust buy index funds" or "if you can't compete, you shouldn't be investing."

That'snot a defense. That's an admission.

Markets don'thave to be this way. The technology exists to give retail investors access toinstitutional-grade analytics. It's just software. It's just data. It's justinterfaces.

The reason it doesn't exist at retail-accessible prices is becausenobody's built it. Because building it threatens existing business models.Because the financial establishment benefitsfrom the current structure.

I'm not going totell you I have the solution. I'm working on it. But I can't promise it willwork. Building software is hard. Buildingfinancial software is harder. Buildingfinancial software that competes with Bloomberg is maybeimpossible.

But what I can tell you with absolute certainty is this: the gap exists.The gap is massive. The gap costs retail investors 6.1% peryear on average according to Dalbar's research.

Over a thirty-year investing career, 6.1% annual underperformance compounds to retiringwith 72% less wealth than you would have with institutional tools.

That'snot a typo. Seventy-two percent.

The playing fieldisn't level. It's tilted. And every time Oracle loses$70 billion in a day and retail investors ask "whathappened," the answer is:

You found outThursday morning. They knew three weeks ago. Because they have tools you don't. And unless that changes, this will keep happening everysingle earnings seasonforever.

That's the truthnobody in financewants to say out loud. I just did.